Is Private Debt Replacing Bank Lending?

Advantages, Challenges, and the Future

By Albertus Rigter, Astra Asset Management

Migration from Banks to the private debt sector

Passionate and talented investors saw an opportunity to make a difference but realised that the framework they were operating on no longer provided them a workable platform. Astra Asset Management UK Ltd was amongst many who have experienced these challenges, which led us to exit from Deutsche Bank in 2012. Many others pioneered before us, and even more followed after us. There is plenty of upside in this movement, which attracts talent and eventually becomes self-fulfilling; more talent leads to improved and streamlined processes, creating greater flexibility and ultimately, better payout. But where are we in the cycle? How much has the private debt sector replaced bank lending? How successful has this journey been for the industry, and is private debt better quality than bank lending?

In this article Albertus Rigter, Partner of Astra Asset Management, shares his perspective on the private debt sector and compares it to the banking sector. Astra Asset Management UK ltd is a London based asset manager with deep expertise across public and private credit markets.

Is private credit a replacement for bank lending?

Our sector likes to stress the difference in terms of quality of loans, process, and many other factors. Just looking at the sheer growth of the private debt sector, the disintermediation becomes obvious. But how different is private credit really from traditional lending? How discerning has our sector been in differentiating the good from the bad?

Let’s simplify first, a loan provided by the private credit sector simply is a bilaterally negotiated loan between parties, except that the lender is not a traditional banking institution. So far, nothing of note.

Of course, a key difference is driven by regulation, such as Basel III or Dodd-Frank, and this naturally has limited the ability of banks to engage in some loan activity that is considered “risky” through the lens of regulation. As a result, the loan approval process involves many committees and ultimately the investment decisions may be based more on regulatory risk weight than genuine fundamental risk-return considerations.

Whether it is the taxi industry, crypto, or the banking industry, disruption usually comes at a time of peak regulation and today, the private debt industry has emerged as a dynamic industry full of entrepreneurship and innovation. We can congratulate ourselves as we feel pretty good about being part of this sector…

But be aware of some of the potential headwinds in private debt

Private credit managers that have emerged since the global financial crisis are buoyed by the benefit of having been able to operate without legacy scandals, fines, litigations, and the cost overheads of dealing with various compliance regimes that banks have faced.

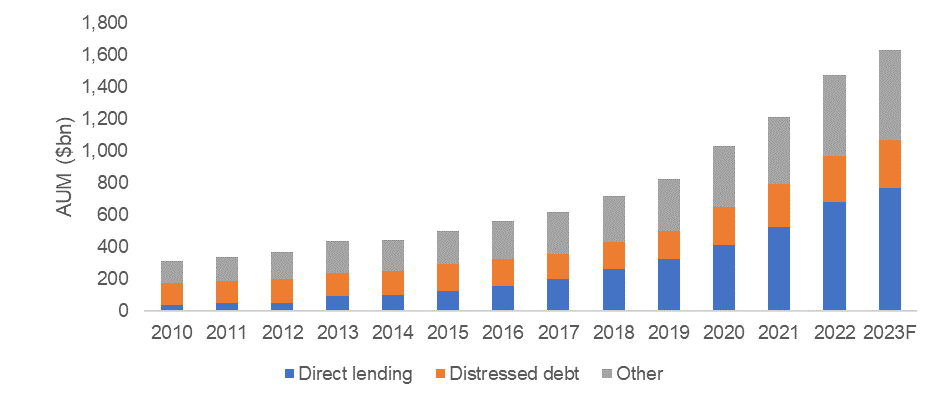

This prosperous environment is also, naturally, where most of the growth has taken place. Just a decade ago the private credit industry was small in the overall context of the financial industry, at just shy of USD 400 billion (one could call this almost a rounding error in the overall credit markets). It is USD 1.6 trillion today1. The growth spurt may have been exacerbated by how the market has evolved; of the top ten private debt firms by size, six are publicly listed. As most of us will know, public shareholders are much more driven by growth in assets than investment performance as the former tends to drive the stock price.

Source: Preqin Pro

With high pressure for returns in a low rate and spread environment, private debt managers generally took on higher corporate credit risk than banks have and largely filled the lending gap. Nonetheless, given the relatively benign credit environment of the past decade, private credit funds generated a track record of limited defaults.

In conclusion, private credit was virtually non-existent during the past crises of 2008, or the European banking crisis of 2012, and provided only a limited amount of capital was available, it could be allocated very selectively. It is therefore extremely difficult to predict how private credit at the current size will fare in a crisis but here is an attempt in identifying a few of the potential headwinds that investors should be aware of:

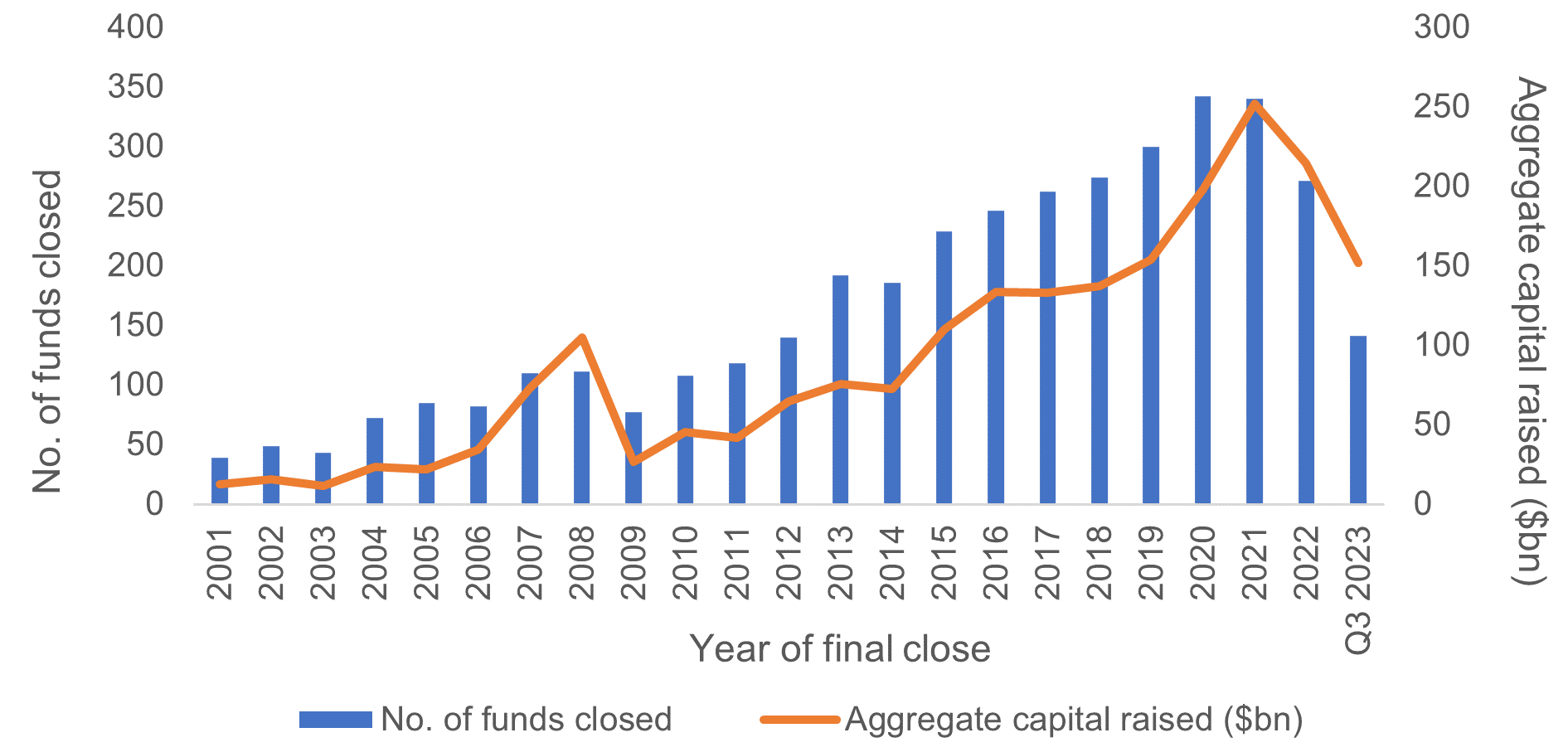

· It has become a more challenging money raising environment. According to Preqin, 20% fewer private debt funds were closed this year compared to 2022 over the same period.2

Source: Preqin Pro

· Deal exits in Private Equity are challenged by a weaker IPO market3 and an almost non-existent SPAC market. Logically, one would expect this to threaten successful amortisation of sponsored private debt loans (a very large part of the private debt market4)

· Provided the massive growth that has taken place in the last ten years, we will be experiencing the first true private debt loan maturity cycle. Having the largest private debt maturity cycle ever taking place in an environment where the corporate costs of capital have multiped will be a challenge for the sector

· There are possible risks resulting from poor loan agreements; the industry growth required increasing deal flow and major concessions have been made by some lenders (usually with private equity sponsors) on protective covenants. Those shortcuts may pose a severe risk and possible loss of capital in a more challenging environment

Combine all these factors, and clearly a more difficult private credit environment is ushered in, and you would likely agree with a preliminary answer to our initial question: is private debt lending of better quality than bank lending has been? Well, the jury is still out!

Now, let’s look at the bright side and how many managers have worked on making private debt a safe alternative to bank lending:

Of course, with the amount of talent and specialisation in our industry, it would be naive to assume that the Private Debt sector will be sitting ducks in a more challenging credit cycle. We’ll review three elements that can mitigate credit risks:

· Structural mitigants

· Solid loan agreements

· Reliable security

Many managers have had a focus on the managing risk through structural mitigants, let’s call them “bells and whistles” which are features designed to protect the lender. Similar to safety features in a car, such as airbags, ESP, and emergency braking systems, these features only manifest when needed but are indeed highly necessary to prevent an accident.

Bilateral loan agreements are the ones negotiated between a borrower and lender and quality of those documents is key to “bad weather” protection. Often, deal flow has only been accessible if one is to accept sponsor lending conditions, but many lenders have been determined to limit concessions and to ensure the loan documents are tailored to their needs rather than the needs of the sponsor or moved away from sponsor backed transactions.

Finally, security; regardless of whether a manager has a focus on cash flow, collateral, or both, it is important to understand how security works. This means understanding what happens in a debt default scenario, and how much and how quickly can one recover value. The success will lie in both the security one has and the experience of recovering the value embedded in that security.

The private debt sector may not have gone through such a cycle yet, but many of the senior players sitting on their teams have.

In conclusion, a bright future for private debt?

Certainly, the private debt sector has the benefit of growing talent, dynamism, flexibility and less regulation, but as pointed out in this article, we can’t say it has been thoroughly tested yet. Therefore, the coming credit cycle may be a good opportunity to differentiate between private debt managers.

The question arises on the issue of scale; will firms that have grown loan books to size of the banks face similar issues as the banks in previous crisis, given their systemic importance and the limited flexibility that results from their size? To what extent were the imposed restrictions on the banking sector an inevitable result of the crisis and will the regulator impose more restrictions on the private sector lending in the same way that UBER faces taxi-industry regulation in many countries now?

But like UBER has transformed the taxi industry, one can argue that Private Lending has an important role in the overall economy as it helps many companies access capital with all the benefits that this entails. It is hard to see this positive trend change.

The next period is prone to be very different from the previous one, given the regime change in cost of capital. Some existing private debt loan portfolios may therefore face challenges and at the same time new opportunities arise. This paper has tried to set out some of the differences, challenges and opportunities between the bank lending and private debt sector, well aware that the reality always plays out differently from what one expects…

About Astra Asset Management UK Ltd

Astra Asset Management UK Limited is an award-winning Asset Manager investing in US & European Asset Backed Credit. It has an eleven-year track record of generating double-digit returns. The firm manages US and European Hedge Fund and Private Credit strategies across the credit spectrum including leveraged loans, mortgage-backed securities, financials, distressed structured credit, real estate lending and asset-based lending. Since its founding in 2012, Astra has emerged as a leading European Alternative Credit Manager and a lender of choice. It has delivered sustained absolute performance across varied credit sectors and delivered sustained performance across market cycles with little to no leverage and limited correlation to credit markets. Astra Asset Management UK Limited is a London-based investment manager authorised and regulated by both the Financial Conduct Authority and the US SEC, in relation to US persons.

Website:

To read more of our insights, visit us here. To see media appearances, click here.

Disclaimer

This article has been prepared by Astra Asset Management UK Limited (Astra). Astra is authorised and regulated by the UK Financial Conduct Authority and is registered as an Investment Adviser with the US Securities Exchange Commission, solely in relation to US persons. The article comprises Astra’s opinion, it is not investment advice and does not comprise a recommendation to enter into any transaction or to follow any investment strategy. Any future-looking statements may comprise hypothetical information, and you should carefully consider the risks inherent to such information when considering this article. Astra will not accept any liability based on the article or any errors or omissions therein. You should obtain professional advice before entering into any transaction or other investment decision. Capital invested is at risk, including of total loss.

Preqin, Future of Alternatives 2028

Preqin, 2024 Global Report: Private Debt, shows the Private Debt direct lending strategies to be around 46% of the 2022 overall Private Debt AUM. Most direct lending is a sponsor-based strategy.